The Corporate Sustainability Reporting Directive (CSRD)

In the European Union, the Corporate Sustainability Reporting Directive (CSRD) has now been brought into law by delegated acts and member state legislation aligned with the common minimum requirements. It requires all large companies (with >250 employees, and the updated thresholds >€45m net annual revenues or >€25m assets on their balance sheet) and listed SMEs, to publish regular reports on their environmental and social impacts.

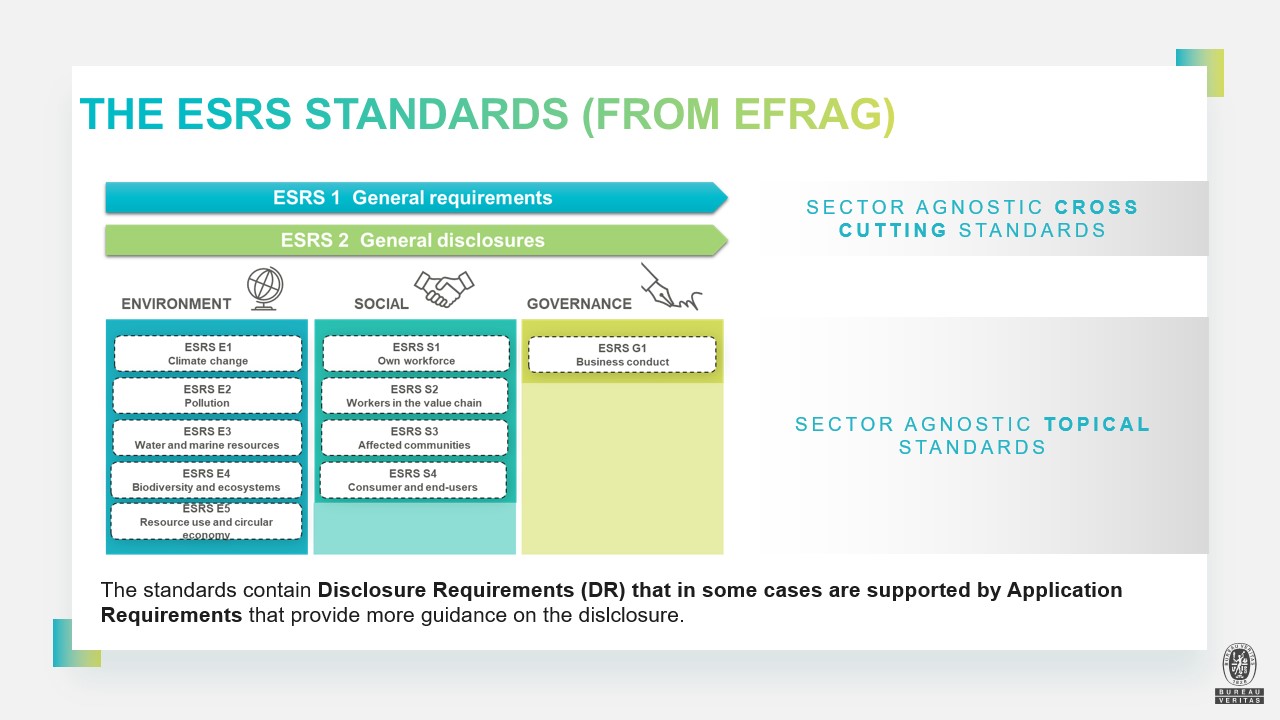

The directive requires companies to disclose information as outlined in the European Sustainability Reporting Standards (the final ESRS are available at this link). This first group of these standards, which apply to all industry sectors, were adopted through specific delegated acts of the European Commission at the end of June 2023. There are twelve standards, two cross-cutting (ESRS 1 and ESRS 2) and ten that are aligned with environmental (ESRSs E1-E5), social (ESRSs S1-S4) and governance (ESRS G1) issues as shown in the diagram.

The information and data reported will be tagged electronically following a specific taxonomy to enable simpler comparison. Independent third-party assurance of sustainability reports published according to the directive will be mandatory in all member states. Bureau Veritas provides assurance of sustainability reports for existing voluntary frameworks such as the Global Reporting Initiative (GRI), AccountAbility (AA1000) and the International Sustainability Standards Board's (ISSB's) S1 and S2 standards, among others.

HOW DOES CSRD IMPACT MY BUSINESS?

-

CLIENT

Image

“My company has made ambitious commitments to sustainability and decarbonization. We’ve made giant strides in reducing our own operational carbon footprint and have enabled our organization to meet aggressive social and governance goals. Now, our next challenge is to support and drive change within our supply chain, so we can meet our increasingly tough targets and commitments for continual improvement.”

-

COMMERCIAL & COMMUNICATION MANAGER

Image

“The market is competitive and we need to demonstrate our sustainability credentials to maintain our edge. It’s not just about compliance anymore, it’s about meeting client expectations. We need to share ESG data with them now, so it makes sense to start formally reporting our sustainability performance now. Third party assurance of our sustainability report will further differentiate us and it will help us have a top class sustainability report in time for CSRD.”

-

INVESTOR RELATIONS MANAGER

Image

“Though my company has been reporting on non-financial matters for a few years, it’s become more focused and it’s now an imperative to be well prepared. My team manages investor enquiries and data demands relating to our corporate ESG credentials for any new investments we make.

Investors are keen to understand the compliance risks and how well the company is prepared to address these new risks.

The differences in investor priorities and regulations by jurisdiction make it complicated to meet all requirements that may impact our future access to capital. Ultimately we will probably have to treat all operations globally with the same rigour demanded by CSRD disclosures.”

-

PURCHASING MANAGER

Image

“I need to develop a process to determine my company’s exposure to environmental, social and governance risks from our suppliers by assessing their ESG practices. Collecting the carbon footprint data of the products and services we buy from them is key to report them under our scope 3 GHG emissions”

-

HUMAN RESOURCES MANAGER

Image

“I will need to collect data for intellectual, human and social disclosures. It requires building systems for the collection of sensitive data. I will need to work on developing an approach to incorporate ESG objectives in the remuneration of staff at all levels. A solid sustainability reporting approach will enable us to continue to attract the best talent”

-

CFO / FINANCE DIRECTOR

Image

“Preparing data that shows the potential sustainability impact of the company on the environment and communities, in addition to the financial impact of sustainability issues on the company is new. My team has to understand how capital providers are considering CSRD in their lending and investment decisions. We are considering putting an internal price on carbon dioxide emissions.

We must define our sustainability reporting boundaries, develop an efficient approach and invest in capabilities to collect data for single electronic reporting. The regulations require limited assurance initially followed by reasonable assurance meaning evidence trials and verification will be required for ESG data. We need to select an external auditor or Independent Assurance Services Provider (IASP) with the right experience. We need a range of auditors to be available to make sure we get a good value, high-quality service.”

-

CEO / EXECUTIVE BOARD MEMBER

Image

“Incorporating sustainability into board reporting with clear responsibility and capability is the new normal. It’s imperative to understand the relationship between sustainability and my company’s business model and strategy. We must ensure our business’ resilience to sustainability risks, and how to ensure our corporate strategy aligns with a decarbonising economy. We have to do our part to limit global warming to 1.5°C.”

-

LEGAL / RISK / COMPLIANCE OFFICER

Image

“As corporate sustainability issues are moving from being voluntary to regulatory, my team needs to understand the detail of the CSRD’s reporting obligations. We are working with risk management systems to understand our ESG obligations and track the implementation and monitoring of our procedures to control those risks and potential impacts.”

-

CHIEF INFORMATION/ CHIEF TECHNOLOGY OFFICER

Image

"My company is a global player with assets on all continents and operations in over 100 countries. We are challenged to find a single approach to our data collection for CSRD. Considering the size of our operations, monitoring and reporting the data will be our ongoing challenge. We need to develop a strategy, and possibly find software solutions, which will make data capture, storage, and reporting in accordance with CSRD easier."